Introduction

1. Overview, status and new discoveries of global conventional oil and gas exploration

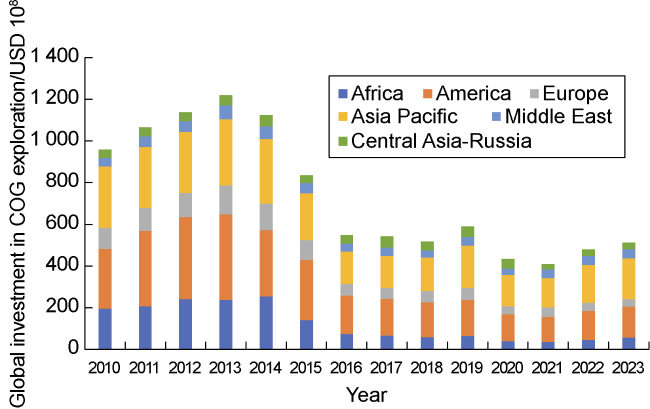

1.1. Change in global investment in conventional oil and gas exploration

Fig. 1. Histogram of year distribution and regional distribution of global investment in COG exploration since 2010 [7]. |

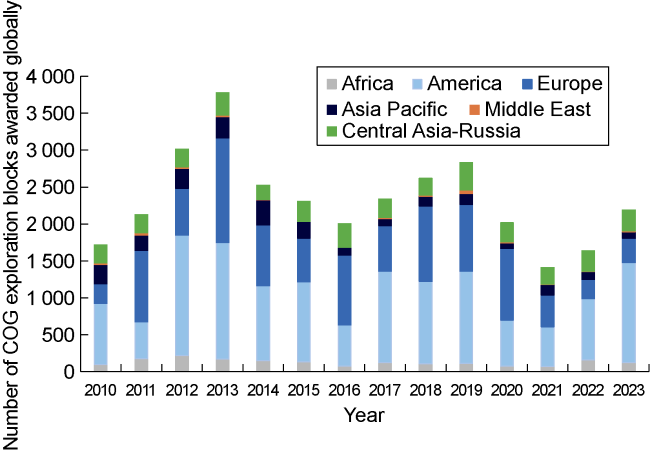

1.2. Award of COG exploration blocks around the world

Fig. 2. Histogram of the year distribution and regional distribution of COG exploration blocks awarded globally [6]. |

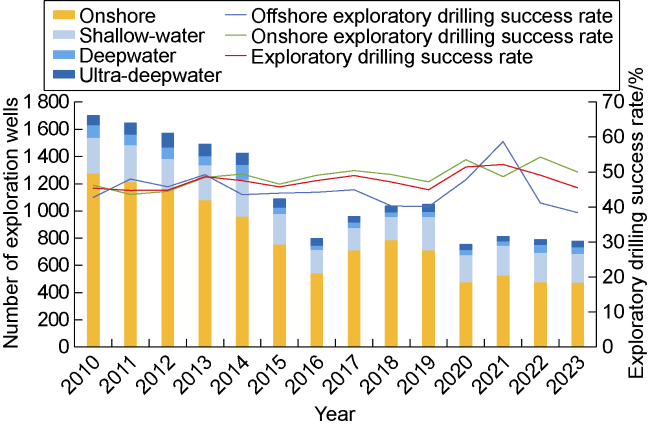

1.3. Change in drilling workload of global COG exploration

Fig. 3. Histogram of the number and success rate of exploration wells drilled around the world during 2010- 2023[6]. |

Table 1. Statistics for the number and success rate of exploration wells drilled globally in 2023 [6] |

| Region | Number of dry wells | Number of gas wells | Number of oil wells | Number of wells with oil and gas shows | Number of wells with undisclosed results | Total number of wells | Success rate/% | Number of high-impact wells | Success rate for high-impact wells/% |

|---|---|---|---|---|---|---|---|---|---|

| Africa | 20 | 14 | 38 | 5 | 19 | 96 | 54.2 | 9 | 22.2 |

| America | 73 | 25 | 75 | 6 | 46 | 225 | 44.4 | 9 | 10.0 |

| Europe | 24 | 20 | 22 | 0 | 10 | 76 | 55.3 | 1 | 100.0 |

| Asia Pacific | 25 | 51 | 41 | 10 | 107 | 234 | 39.3 | 6 | 42.9 |

| Middle East | 5 | 7 | 22 | 0 | 42 | 76 | 38.2 | 2 | 50.0 |

| Central Asia-Russia | 1 | 9 | 30 | 0 | 31 | 71 | 54.9 | 0 | 0 |

| Total | 148 | 126 | 228 | 21 | 255 | 778 | 45.5 | 27 | 29.6 |

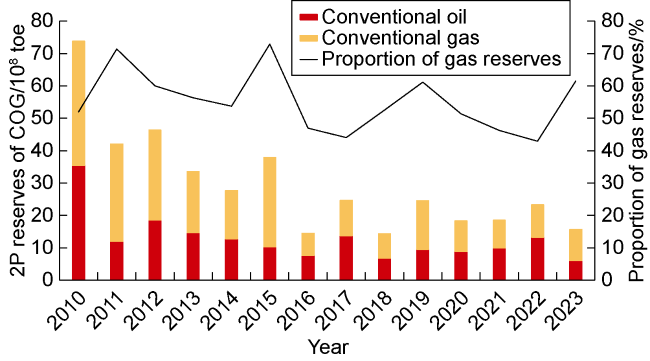

1.4. New global COG discoveries

Fig. 4. Histogram of global recoverable COG reserves discovered during 2010 to 2023 [6]. |

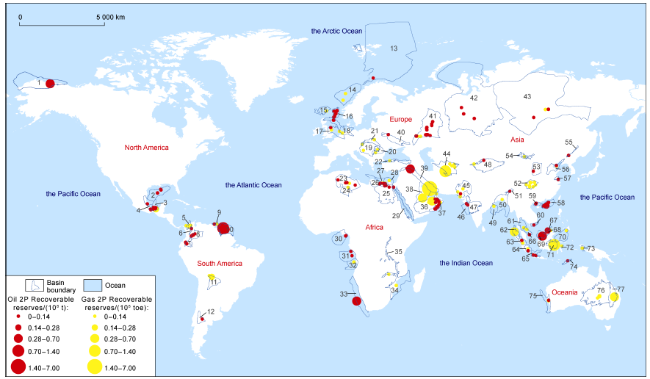

Fig. 5. Distribution of new oil and gas discovered around the world in 2023 [6].1. North Slope Basin; 2.Deep Water Gulf of Mexico Basin; 3. Sureste Basin; 4. Veracruz Basin; 5. Lower Magdalena Basin; 6. Middle-upper Magdalena Basin; 7. Putumayo Basin; 8. Llanos Basin; 9. Trinidad Basin; 10.Guyana Basin; 11. Chaco Basin; 12. Neuquen Basin; 13. Barents Sea Platform; 14. Voring Basin; 15. Faroes-West Shetland Basin; 16. North Sea Basin; 17. Anglo-Dutch Basin; 18. Northwest German Basin; 19. Pannonian Basin; 20. South Carpathian Basin; 21. North Carpathian Basin; 22. Pontids Basin; 23. Tri-Ghadames Basin; 24. Illizi Basin; 25. Upper Egypt Basin; 26. Cyrenaica Basin; 27. Northern Egypt Basin; 28. Nile Delta Basin; 29. Red Sea Basin; 30.Niger Delta Basin; 31. Lower Congo Basin; 32. Kwanza Basin; 33. Southwest African Coastal Basin; 34. Mozambique Basin; 35. East African Rift System; 36. Rub' Al Khali Basin; 37. Oman Basin; 38. Central Arabian Basin; 39. Zagros Basin; 40. Dnieper-Donets Basin; 41. Volga-Urals Basin; 42. West Siberian Basin; 43. East Siberian Basin; 44. Amu-Darya Basin; 45. Indus Basin; 46. Bombay Basin; 47. Deccan Basin; 48.Tarim Basin; 49. Mahanadi Basin; 50. Bengal Basin; 51. Assam Basin; 52.Sichuan Basin; 53.Ordos Basin; 54. South Gobi Basin; 55. Yilan-Yitong Basin; 56. Bohai Gulf Basin; 57.Subei Basin; 58. Pearl River Mouth Basin; 59. Beibu Gulf Basin; 60. Cuu Long Basin; 61. Gulf of Thailand Basin; 62. North Sumatra Basin; 63. Central Sumatra Basin; 64. South Sumatra Basin; 65. West Java Basin; 66. Malay Basin; 67.Northwest Sabah Platform; 68. Brunei-Sabah Basin; 69.Zengmu Basin; 70. Celebes Basin; 71. Kutei Basin; 72. Banggai Basin; 73. Bintuni Basin; 74. Timor Basin; 75. Perth Basin; 76. Eromanga Basin; 77. Bowen-Surat Basins |

Table 2. Statistics of the top ten COG discoveries in the world in 2023 [6] |

| Country | Field | Operator (oil company) | Scale | Area | Field type | Basin | Formation | 2P Recoverable reserves/(108 toe) |

|---|---|---|---|---|---|---|---|---|

| Iran | Shahini 1 | NIOC | Large | Onshore | Gas field | Zagros Basin | Upper Permian- Lower Triassic | 3.58 |

| Iran | Cheshmeh Shoor 1 | NIOC | Large | Onshore | Gas field | Amu Darya Basin | Upper Triassic | 1.16 |

| Indonesia | Geng North 1 | Eni | Large | Ultra-deepwater | Gas field | Kutai Basin | Upper Miocene- Pliocene | 0.83 |

| Guyana | Lancetfish 1 | ExxonMobil | Large | Ultra-deepwater | Oilfield | Guyana Basin | Upper Cretaceous | 0.79 |

| Guyana | Fangtooth SE 1 | ExxonMobil | Medium | Ultra-deepwater | Oil and gas field | Guyana Basin | Upper Cretaceous | 0.54 |

| USA | Hickory | 88Energy | Medium | Onshore | Oil and gas field | Alaska North Slope Basin | Upper Cretaceous | 0.54 |

| Namibia | Jonker 1X | Shell | Medium | Ultra-deepwater | Oil and gas field | Southwest African Coastal Basin | Upper Cretaceous | 0.53 |

| Suriname | Roystonea 1 | Petronas | Medium | Deepwater | Oil and gas field | Guyana Basin | Upper Cretaceous | 0.45 |

| Turkey | Sehit Aybuke Yalcin | TPAO | Medium | Onshore | Oilfield | Zagros Basin | Cretaceous | 0.45 |

| Indonesia | Layaran 1 | Mubadala | Medium | Deepwater | Gas field | North Sumatra Basin | Lower Miocene | 0.42 |

Note: The recoverable reserves (toe) of large, medium, and small oil and gas fields are more than 0.69×108 t, (0.14-0.69)×108 t, and less than 0.14×108 t, respectively. |

2. Overview of global exploration of unconventional oil and gas and associated resources

2.1. Global unconventional oil and gas exploration

2.2. Exploration of associated resources around the world

2.2.1. Natural hydrogen

2.2.2. Helium

3. Characteristics of new oil and gas discoveries globally

3.1. Large- and medium-sized oil and gas fields contribute greatly to the total newly discovered reserves

3.2. The onshore reserves newly discovered are basically equal to the newly discovered offshore reserves

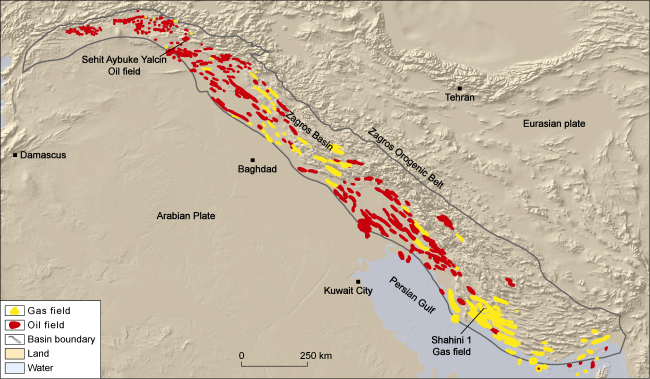

3.3. Fine exploration in mature basins has achieved remarkable results

Fig. 6. Distribution of oil and gas fields in the Zagros Basin of Iran in the Middle East. |

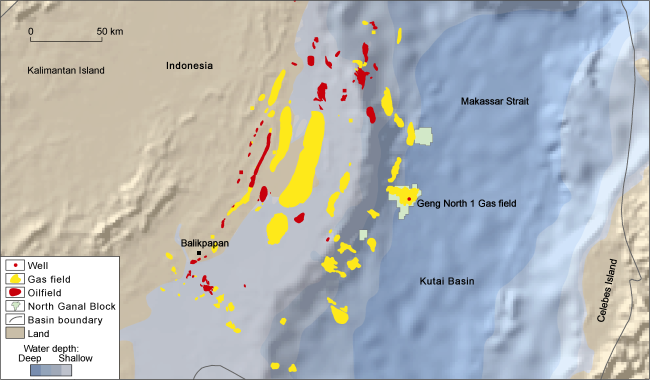

3.4. Deepwater areas have broad exploration prospects

Fig. 7. Current status of oil and gas exploration in the Kutai Basin of Indonesia in the Asia Pacific region and the location of Geng North 1 Gas Field in Indonesia, Asian-Pacific. |

3.5. The UOG industry is developing rapidly, and oil companies are accelerating their strategic planning

3.5.1. Middle East

3.5.2. North Africa

3.5.3. West Siberian Basin, Russia

4. Trends in the exploration of oil, gas and associated resources by the seven major international oil companies

4.1. Change in investments by the seven major international oil companies

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

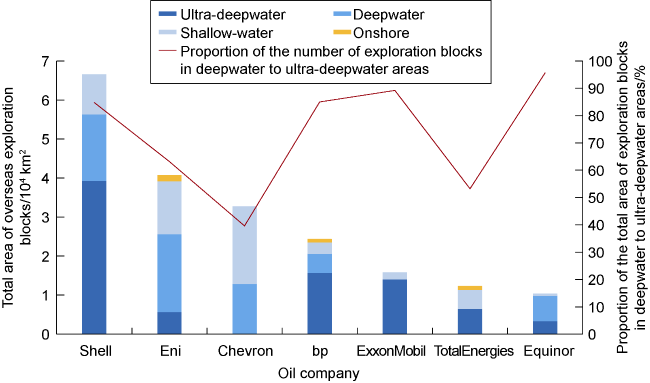

Fig. 8. Histogram of the distribution (onshore/offshore) of overseas exploration blocks acquired by the seven major international oil companies in 2023 [6]. |

4.2. Similarities and differences of exploration blocks acquired by the seven major international oil companies

4.3. Situation of UOG exploration by the seven major international oil companies

4.4. Trends in the development of associated resources by the seven major international oil companies

5. Development strategies in overseas hydrocarbon exploration

5.1. Continue to invest in the upstream exploration

5.2. Continue to carry out oil and gas exploration

5.2.1. Deeply explore mature basins

5.2.2. Closely follow hotspot basins

5.2.3. Gain access to frontier basins as soon as practicable

Table 3. Favorable COG exploration areas along the Two Rims |

| Country | Basin name | Basin type | Area | Undiscovered recoverable resources/(108 toe) | Key zones | |

|---|---|---|---|---|---|---|

| Oil | Gas | |||||

| Mozambique | Mozambique Basin | Passive margin basin | Frontier | 4.0 | 23 | Jurassic biogenic reefs, Cretaceous-Paleogene slope fans |

| Somalia | Somali Basin | Passive margin basin | Frontier | 3.0 | 32 | Cretaceous-Paleogene slope fans/basin-floor fans |

| Benin | Benin Basin | Passive margin basin | Frontier | 6.4 | Upper Cretaceous gravity flow sandstones | |

| Malta/Liberia | Senegal River Basin | Passive margin basin | Hotspot | 6.0 | 23 | Upper Cretaceous basin-floor fans |

| Namibia | Orange Basin | Passive margin basin | Hotspot | 15.0 | 10 | Upper Cretaceous slope fans/Lower Cretaceous basin-floor fans |

| Brazil | Santos Basin | Passive margin basin | Hotspot | 133.0 | 21 | Pre-salt biogenic reefs/post-salt gravity flow sandstones |

| Campos Basin | Passive margin basin | Hotspot | 110.0 | 37 | Pre-salt biogenic reefs/post-salt gravity flow sandstones | |

| Foz do Amazonas Basin | Passive margin basin | Frontier | 12.0 | 2 | Upper Cretaceous gravity flow sandstones | |

| Argentina | Colorado River Basin | Passive margin basin | Frontier | 11.0 | 1 | Jurassic-Cretaceous rifts, slope fans, anticlines, etc. |

| Argentine Coastal Basin | Passive margin basin | Hotspot | 18.0 | 6 | Upper Cretaceous slope fans/Lower Cretaceous basin-floor fans | |

| Suriname | Guyana Basin | Passive margin basin | Hotspot | 14.0 | 2 | Upper Cretaceous slope fans |